Bad Credit Payday Loans

Table of Contents

- The True Meaning of ‘No Credit Check’ Payday Loan

- Interest Rates on Payday Loans For People With Bad Credit

- What does it mean to have bad credit? The FICO score

- Is My Credit Score Bad?

- Your Credit Score vs Credit History

- Is The Situation Better in States With Caps on Payday Loan APR?

- Learn to Calculate Your Bad Credit Loan APR

- Avoid Bad Credit Loan Scams

34% of adults in the US have a bad or below-average credit score. The current crisis is likely to increase the percentage of people with bad credit.

For borrowers with a low credit rating, it becomes harder and harder to get a loan from a regular lender. These people easily get into the vicious circle of borrowing and constant debt.

In fact, an average payday borrower spends more than 6 months each year in debt, taking out 10 payday loans. Most alarmingly, people often use payday loans to pay rent and utility bills – simply because they have no other source of money.

A staggering 80% of all payday loans are taken out within 2 weeks of paying off the previous one.

A single figure shows how ubiquitous payday loans are: there are more payday loan storefronts in the US than there are McDonald’s restaurants. Since they are everywhere, a payday loan often seems like the obvious solution for borrowers with a bad or no FICO credit score.

The True Meaning of ‘No Credit Check’ Payday Loan

If you have a bad credit score, you might be attracted by offers of payday loans with no credit checks. In reality, every lender – including a payday loan shop – will conduct a check of some sort. The difference is that it will be a so-called ‘soft’ check, not a ‘hard’ check.

1. Hard credit check, or ‘hard pull’. When a lender pulls your credit history from one of the 3 big bureaus (Experian, Equifax, TransUnion), it’s called a hard check. The lender can only do it with your permission and in connection with a loan you requested.

Every such inquiry leaves a temporary mark on your credit file. On average, it’s five points per check. This ‘credit check penalty’ only lasts for a few months.

However, if you apply for several loans within a short time, the cumulative effect can be serious. Apart from the damage to your score, a lender will see multiple hard checks on your file and think that you must be in dire need of money. That can classify you as a higher-risk borrower than you really are and result in worse interest rates.

2. Soft credit check. This is any kind of check that doesn’t include an official inquiry to the 3 major bureaus and doesn’t have any impact on your credit score. It doesn’t require your permission, either. The lender doesn’t have to inform you about a soft check. However, you’ll find it if you check your credit report.

Payday lenders normally conduct only soft checks. So the fact that you asked for a payday loan won’t damage your FICO score in any way.

This is a serious advantage. If you already have bad credit, at least a payday loan won’t make it worse. On the other hand, it won’t make it better, either, even if you pay off the loan on time.

Remember that if you fail to repay a payday loan, your case will go to debt collectors, and then your credit score can indeed suffer.

Interest Rates on Payday Loans For People With Bad Credit

A payday loan is the easiest kind of loan to get. Most of the time you’ll need to prove that you’re employed and show your last payment check. That’s why many lenders advertise approval rates of up to 97%.

However, most payday lenders’ customers are categorized as high-risk. Most have a low credit rating – or even none at all, as is the case with very young people. The average annual wage for such borrowers is $30,000.

To protect themselves from the high risk of default, the lenders set very high interest rates – though they won’t necessarily seem so high at first glance. On average, you’ll pay between $10 and $30 to borrow $100 for 14 days.

$10-$15 doesn’t seem like a huge price to pay when you need money urgently. However, you need to calculate the annual rate (APR) to know the real cost of your loan. According to the analysts of the Federal Reserve Bank of St Louis, the average annual interest rate on payday loans is a whopping 391%.

For comparison: APRs on personal loans vary from 14% to 35%, and the average rate for credit cards is 16%.

What does it mean to have bad credit? The FICO score

When we talk about bad credit, we usually mean low FICO score. Circa 90% of major lenders use FICO. The name of the model is an abbreviation for Fair Isaac Corporation – a US data analytics company that created it.

Another reasonably popular model is VantageScore, developed by the 3 leading credit bureaus – Experian, Equifax, and TransUnion.

Your FICO score is calculated based on these elements:

- 35%: your payment history;

- 30%: how much money you owe already;

- 15%: credit history length;

– 10%: how often you ask for and get new loans. This has to do with hard credit checks on your file (read on to find out more).

– 10%: how varied your credit is (loans, mortgage, credit card, instalment loans, etc.).

Is My Credit Score Bad?

A FICO score can go from 300 to 850. According to Fair Isaac Corporation (FICO), borrowers fall into the following ranges:

- Less than 580 (16% of borrowers). Bad – far below the average and high risk for lenders. Payday loans are just about the only loans one can get.

- From 580 to 669 (18% of borrowers). Fair – below average, but you can get some loans, including payday loans. Don’t expect a good rate, though.

- From 670 to 739 (21% of borrowers). Good, around and above the average in the US.

- From 740 yo 799 (25% of borrowers). Very good – above average and low risk for lenders.

- Over 800 (20% of borrowers). Exceptional. These borrowers get the best rates.

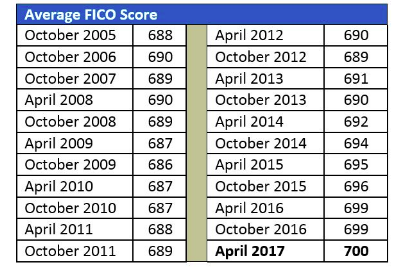

The average credit score has been growing for many years and now stands at 703.

Your Credit Score vs Credit History

When a lender conducts a credit check, they don’t just look at your FICO score. They also pull credit reports from Experian, Equifax and/or TransUnion.

The 3 large credit bureaus collect information about your borrowing history from different lenders: banks, credit unions, credit card companies, car dealers, etc. With these data, they compile detailed credit reports on you.

These reports are very detailed: the lender will see every late payment you’ve made. Each of the bureaus also calculates its own credit score, though it usually correlates with FICO.

Two people with the same credit score can have very different credit histories. That’s why many lenders include both FICO and bureaus’ reports in their credit checks. A lender can consult all three or just one.

Still, you should worry about your FICO score more than the reports. In many cases, such as mortgages, there’s a minimum credit score below which you can’t get a loan – no matter what your credit report says.

Is the Situation Better in States With Caps on Payday Loan APR?

Some states have imposed a maximum APR that can be charged on payday loans. It would seem like the borrowers in these states are in a better position, but the reality is more complicated.

A recent study looked at the state of Rhode Island, where the maximum APR was lowered from 390% ($15/mo for each $100 borrowed) to 260% ($10/mo for each $100).

The idea was to make payday loans less predatory. However, there were serious negative side effects. People with bad credit saw that payday loans became cheaper and began to get them more often. A higher percentage of loans were rolled over (extended for the subsequent month), so the overall amount of borrowers paid in fees grew.

Learn to Calculate Your Bad Credit Loan APR

Here’s a simple example. Let’s say you’re borrowing $100 for 14 day, and the total charge (all the fees you’ll need to pay) is $16.

- Divide the total fees by the loan amount:

$16/$100=0.16, or 16%. - Multiply the result by 365:

0.16*365=58.4 - Divide this result by the loan term in days (in our case 14 days): 58.4/14=4.17

- Multiply by 100%:

4.17*100%=417%

That’s the real interest rate you’ll be paying: 417% a year.

It won’t become a heavy financial burden if you pay off the loan after 2 weeks. But if you keep rolling it over, the costs will quickly accumulate – especially since extra rollover charges will be applied.

Avoid Bad Credit Loan Scams

If you still feel like you need a payday loan, do a thorough research first. Scams are rife in this market. The following signs point to a scam:

– Request for a downpayment. A scammer will ask you to send a small sum to secure the loan – usually around $50. It can be called collateral, insurance charge or origination fee.

Obviously, you won’t get any loan: the scammer will simply disappear with your money. And since the amount is small, you probably won’t go to the police, either: that’s what allows such scammers to thrive.

This scheme is called an advance fee loan, and it’s illegal. The US law doesn’t allow lenders to charge any fee before their client receives the money.

– Request for sensitive personal information before your loan is approved. If you haven’t seen the contract yet, but the lender is already asking for your social security number, it’s a bad sign. Definitely don’t provide any data over the phone. Identity theft is very common. Chances are that scammers just want to sell your bank account number of SSN on the black market.

Payday loans can be the only choice for people with a bad credit score who need money urgently. But before you request one, make sure to compare several loan stores near you.

Check or calculate the APR for each and take note of any late charges and rollover fees. Remember: a payday loan is a short-term credit instrument. If you keep extending one, you’ll end up paying much more than what you obtained in the first place.